Czech ESOP reform 2026: finally, stock options that work for startups

Employee stock option plans (ESOPs) are the go-to tool for startups worldwide to attract and keep top talent. In Czechia, though, the system hasn’t worked. Startups could grant options, but without any tax benefits. Most ended up using phantom shares as a workaround that felt like equity but was taxed as salary.

That changes in January 2026. A long-awaited reform finally introduces qualified employee options with clear rules and major tax advantages. For Czech startups, it’s a breakthrough: ESOPs become usable, predictable, and competitive on a global level.

Why the old system failed?

Until now, options came with more pain than gain:

- Employees were taxed at exercise, often without liquidity to cover the bill. Technically, there was a possibility to defer the payment, but it was rarely used in practice. Startups faced uncertainty about when the tax would be triggered (e.g. an employee changing tax residency without the company’s knowledge), which could leave the company exposed to unpaid tax and penalties.

- Social and health contributions applied, pushing the burden to around 50%.

- No clear legal framework existed, just a patchwork of interpretations.

No surprise many founders defaulted to phantom (virtual) shares. They looked like equity but were treated as salary. Employees missed out on ownership, founders missed out on a true long-term incentive. And everybody missed out on tax benefits.

What changes in 2026?

The reform introduces qualified employee options with straightforward, startup-friendly rules.

The biggest shifts:

- Tax deferral → up to 15 years or until employees sell shares.

- No exit tax on relocation → moving abroad won’t trigger an immediate tax bill.

- Simpler reporting → grants and exercises must be reported to the tax office within 20 days.

- Social and health relief → contributions generally don’t apply.

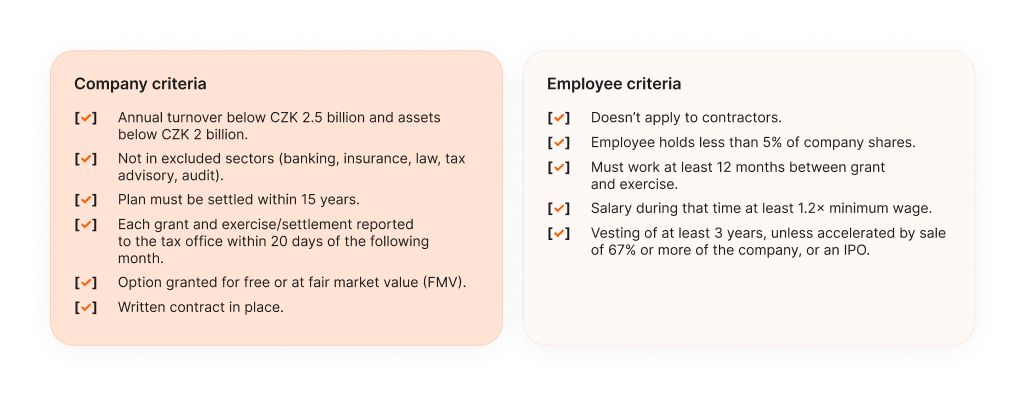

Who qualifies?

To use the new regime, both the company and the employee must meet specific conditions.

How will taxation work?

The reform flips the old model on its head:

- Before → Options were taxed like salary at exercise (income tax and social & health contributions; effective burden up to 52%), collected by the employer through payroll, even when shares couldn’t be sold by the employee to cover the tax bill.

- Now → Taxation is deferred until sale (or after 15 years if still held). Rates are 15–23%, and the burden shifts from employer to employee.

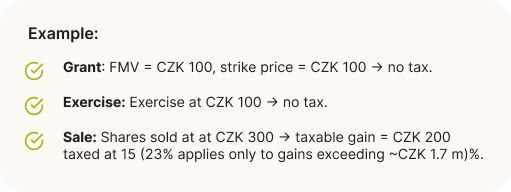

Step by step after the 2026 reform:

- Grant → No tax if strike (exercise price) equals FMV.*

- Exercise → No tax, if strike (exercise price) at grant equals FMV.*

- Sale (or after 15 years) → Tax due at 15–23% on the gain. The taxable gain = sale price (exit) – strike price if the strike price was at least equal to the fair market value (FMV) at grant.*

*If strike price at grant was below FMV, the difference (FMV - strike price) is taxed right away as salary income, with income tax plus social and health contributions (effective burden can reach ~52%).

Why this matters and who benefits?

- Founders and startups → Equity finally becomes a practical hiring and retention tool, without payroll shocks at exercise. From 2026, the tax liability shifts to employees and only arises at sale. You can grant equity without draining company cash and stay competitive with international peers.

- Employees → No more tax on “paper gains.” Instead, tax applies only when shares are sold (or after 15 years) at 15–23%. Social and health contributions generally don’t apply, so equity becomes a genuine benefit, not a liability.

- Investors → A cleaner, better-aligned cap table. Everyone is incentivized to grow long-term value. The one caveat: qualified options don’t enjoy the usual capital gains exemption at exit.

In a nutshell

Until now, ESOPs in Czechia were little more than a symbolic gesture. There were complex, risky, and tax-unfriendly. From January 2026, that changes. With qualified employee options, startups finally get a clear, predictable framework that defers taxation, removes payroll shocks, and puts equity on global terms. For founders, that finally means a real tool to attract and retain talent. And for the Czech startup scene, it’s the reform we’ve been waiting for.

Turn the new rules into your advantage. Book a call now.

- Why the old system failed?

- What changes in 2026?

- Who qualifies?

- How will taxation work?

- Why this matters and who benefits?